According to new data issued by the Office of National statistics (ONS) a quarter of neighbourhoods in England and Wales were off-limits to many prospective homeowners last year because average income in these areas was below the level needed to buy an entry-level property.

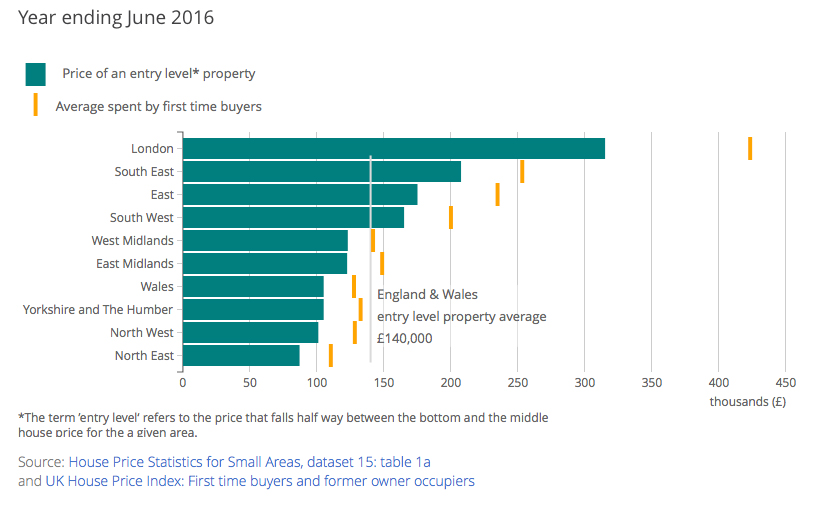

According to analysis, the cost of an entry-level property on average across England and Wales has increased by almost 20% in the last decade, to £140,000. For new properties, the price was nearly £180,000. The data suggests that home-ownership prospects varied across the country.

Those in England who succeeded in making it onto the property ladder in 2016 paid on average more than £198,0005. Would-be homeowners in London faced more of an uphill climb, with the average value paid by first-time buyers over £423,000.

First-time buyers entering the property market typically purchased homes for more than the average entry-level house price where they live. This was the case in all English regions and in Wales, showing that those who did manage get onto the property ladder for the first time could actually afford more than the cost of an entry-level property.

However, this doesn’t reflect those people who couldn’t afford to buy their first home. Assuming a 15% deposit, new buyers in London could require a household income of nearly £60,000 and savings of £55,000, challenging for many.

A typical household in England and Wales could need an income of £26,444 in order to borrow enough for an entry-level property, however this figure varied greatly within regions.

What areas were the most and least affordable?

Some of the least affordable areas were in London. In general these areas were estimated to have higher than average household income, but house prices were significantly higher than in other regions of England and Wales.

A neighbourhood in Wandsworth, London, for example had an estimated average annual household income of £89,223, but the estimated income required for an entry-level property was £127,689.

The most affordable neighbourhoods were generally in the north of England and parts of Wales. Many of the neighbourhoods in these areas had relatively low average income, but had more affordable housing.

London and its surrounding neighbourhoods had some of the most extreme gaps between average income and the income required to buy property, but relatively unaffordable areas were by no means limited to the city.

Entry-level properties across much of the south coast of England could be relatively unaffordable for households on average income. The Foxholes neighbourhood in Poole for example had an average household income of just under £35,000, but the income required to buy an entry-level property was just under £40,000.

Parts of Oxfordshire and its neighbouring counties also had a large number of relatively unaffordable areas. The Littlemore neighbourhood in the city of Oxford had an average household income just over £39,000 but the income required to buy an entry-level property was over £45,000.

The associated costs of moving home

A deposit, stamp duty, legal fees and other associated moving costs are all considerations when buying a home, requiring many first-time buyers to have substantial savings or other sources of funding such as from parents. The recent Government Housing White Paper for England set out ways in which first-time buyers will be supported in saving for a deposit, such as through the Lifetime Individual Savings Account (ISA) which offers a 25% bonus on top of savings towards the purchase of a first home.

With the average cost of an entry-level home in England and Wales being £140,000, prospective buyers could require £300 stamp duty, an estimated £2,000 for legal and moving costs and £21,000 for a 15% deposit, coming to £23,300 in total.

The savings needed to purchase an entry-level property varied disproportionately to house prices between different areas. Stamp duty on more expensive properties can add thousands of pounds on top of a 15% deposit, whereas buyers in areas where an entry-level property costs less than £125,000 are not required to pay any stamp duty.

A neighbourhood in Pendle just north of Burnley, for example, required those buying an entry-level property to have typical savings of £7,625 for a 15% deposit and other costs due to the low cost of an entry-level property. This represents about 3 months’ average income for a household in this area.

In contrast, buyers in one neighbourhood in Reading could owe stamp duty of £5,375 on an entry-level property, on top of a much larger deposit of £46,125. With other associated fees, buyers in this area could need savings of £53,500. This represents more than one year’s income for an average household in this area, and other research suggests it could take a lower income household much longer than this to save for a first home

Help and advice for families

Here at The Financial Planning Group we are specialists in helping families and home owners of all ages find the perfect mortgage deal – we can even secure a mortgage deal six months ahead of your current deal ending – which makes it possible for our clients to reserve the best rates regardless of what the market does in that period.

If you would like to speak about your mortgage or re-mortgage, and secure one of the record low deals that are currently available, please feel call Steve Padgman on 020 8614 4782 or email Steve.Padgham@fpgonline.co.uk